Economic data are frequently generated by stochastic processes that can be modeled as realizations of random functions (functional data). This paper adapts the specification test for functional data developed by Bugni, Hall, Horowitz, and... more

Statistical inference for unknown distributions of statistics or estimators may be based on asymptotic distributions. Unfortunately, in the case of dependent data the structure of such statistical procedures is often ineffective. There... more

Forecasts from a univariate autoregressive model estimated by OLS are unbiased, irrespective of whether the model fitted has the correct order; this property only requires symmetry of the distribution of the innovations. In this paper,... more

We study two Durbin-Watson type tests for serial correlation of errors in regression models when observations are missing. We derive them by applying standard methods used in time series and linear models to deal with missing... more

This paper provides a simple method to estimate both univariate and multivariate MA processes. Similar to Durbin's method, it rests on the recursive relation between the parameters of the MA process and those of its AR representation.... more

This paper provides a simple method to estimate both univariate and multivariate MA processes. Similar to Durbin's method, it rests on the recursive relation between the parameters of the MA process and those of its AR representation.... more

This paper provides a simple method to estimate both univariate and multivariate MA processes. Similar to Durbin's method, it rests on the recursive relation between the parameters of the MA process and those of its AR representation.... more

In this paper we provide an asymptotic theoretical power comparison in the Bahadur sense, between the portmanteau and Breusch-Godfrey Lagrange Multiplier (LM) tests for the goodness-of-fit checking of vector autoregressive (VAR) models.... more

proposed an efficient method to estimate the conditional variance of heteroskedastic regression models. Chen, Cheng, and Peng (2009) applied variance reduction techniques to the estimator of Fan and Yao (1998) and proposed a new estimator... more

The article discusses statistical inference in parametric models for panel data. The models feature dynamics of a general nature, individual effects, and possible explanatory variables. The focus is on large-cross-section inference on... more

We propose tests of the null of spurious relationship against the alternative of fractional cointegration among the components of a vector of fractionally integrated time series+ Our test statistics have an asymptotic chi-square... more

This paper proposes bootstrap assisted specification tests for the autoregressive fractionally integrated moving average model based on the Bartlett Tp-process with estimated parameters whose limiting distribution under the null depends... more

This paper analyzes the classical linear regression model with measurement errors in all the variables. First, we provide necessary and sufficient conditions for identification of the coefficients. We show that the coefficients are not... more

The research is aimed at exploring Foreign Direct Investment and its impact on economic growth of Nigeria. The study covers 31-year period between 1985-2016. Simple ordinary least-square regression model is used to measure the effects and... more

and the participants of the 21 st NZESG Meeting for their useful comments. We also thank Mardi Dungey (

This paper proposes a robust moment selection method aiming to pick the best model even if this is a moment condition model with mixed identification strength, that is, moment conditions including moment functions that are local to zero... more

and the participants of the 21 st NZESG Meeting for their useful comments. We also thank Mardi Dungey (

It is well-known that if the forcing variable of a present value (PV) model is an integrated process, then the model will give rise to a particular cointegrating restriction. In this paper we demostrate that if the PV relation is exact,... more

In this paper we propose a new nonparametric test for conditional heteroskedasticity based on a measure of nonparametric goodness-of-fit (R2) that is obtained from the local polynomial regression of the residuals from a parametric... more

We consider the problem of combining forecasts from two different levels ~called "macro" and "micro"!, where we have access to the forecasts and their precisions but not to the full data set+ We develop a theoretical framework and provide... more

We consider the Breitung (2002, Journal of Econometrics 108, 343–363) statistic ξn, which provides a nonparametric test of the I(1) hypothesis. If ξ denotes the limit in distribution of ξn as n → ∞, we prove (Theorem 1) that 0 ≤ ξ ≤ 1/π2,... more

Any opinions expressed in this paper are those of the author(s) and not those of IZA. Research published in this series may include views on policy, but IZA takes no institutional policy positions. The IZA research network is committed to... more

A formal statistical test of stationary-ergodicity is developed for known Markovian processes on ℝd This makes it applicable to testing models and algorithms, as well as estimated time series processes ignoring the estimation error. The... more

It is known that Efron's resampling bootstrap of the mean of random variables with common distribution in the domain of attraction of the stable laws with infinite variance is not consistent, in the sense that the limiting distribution of... more

We study the problem of identifying a forecaster's loss function from observations on forecasts, realizations, and the forecaster's information set. Essentially different loss functions can lead to the same forecasts in all situations,... more

The paper investigates the relationship between inflation and unemployment in the South African setting, encompassing a comprehensive analysis of historical, theoretical, and empirical evidence. Existing literature surveys demonstrate... more

Many popular estimators for duration models require independent competing risks or independent censoring. In contrast, copula based estimators are also consistent in presence of dependent competing risks. In this paper we suggest a... more

The order of integration is valid to characterize linear processes; but it is not appropriate for non-linear worlds. We propose the concept of summability (a re-scaled partial sum of the process being Op(1)) to handle non-linearities. The... more

Some statistical properties of a vector autoregressive process with Markov-switching coefficients are considered. Sufficient conditions for this nonlinear process to be covariance stationary are given. The second moments of the process... more

The online meta-learning framework has arisen as a powerful tool for the continual lifelong learning setting. The goal for an agent is to quickly learn new tasks by drawing on prior experience, while it faces with tasks one after another.... more

Reduced-rank regression is a dimensionality reduction method with many applications. The asymptotic theory for reduced rank estimators of parameter matrices in multivariate linear models has been studied extensively. In contrast, few... more

This paper studies the two-step sieve M estimation of general semi/nonparametric models, where the second step involves sieve estimation of unknown functions that may use the nonparametric estimates from the …rst step as inputs, and the... more

In this study, we consider preliminary test and shrinkage estimation strategies for quantile regression models. In classical Least Squares Estimation (LSE) method, the relationship between the explanatory and explained variables in the... more

In a classical regression model, it is usually assumed that the explanatory variables are independent of each other and error terms are normally distributed. But when these assumptions are not met, situations like the error terms are not... more

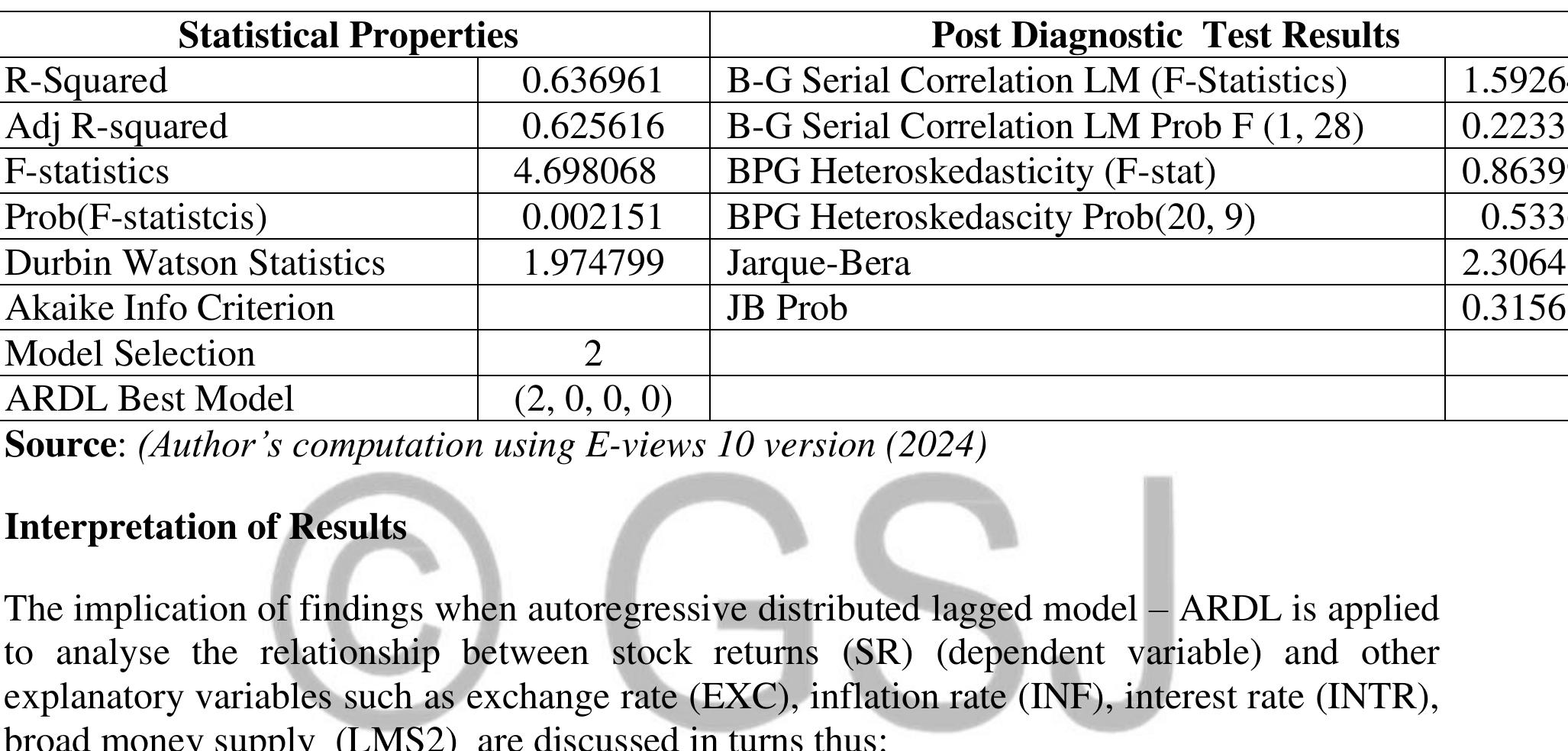

This study has empirically investigated the impact of macroeconomic variables on stock returns in Nigeria. The method of analysis used in this study is Autoregressive Distributed Lag (ARDL) model. The study spanned from 1987 up to 2022.... more

By pointing out the spurious regression problem, Granger and Newbold ~1974! have shown the importance of stochastic trends in time series data in the context of linear regression models+ At the time, removing trends by differencing was... more

In this note we show that, when the true data generating process is a stationary one around a constant term with a break, the stationarity test of Kim ~2000, Journal of Econometrics 95, 97-116! against the alternative hypothesis of change... more

duals or institutions. Indeed, as long as public and private agents must make decisions that require judgement as to the future of economic events, forecasts will not only continue to be made, but acted upon. Considered as a branch of... more

This paper extends the simple threshold regression framework of Hansen (2000) and Caner and Hansen (2004) to allow for endogeneity of the threshold variable. We develop a concentrated least squares estimator of the threshold parameter... more

We consider a parameter estimation problem for a diffusion with killing, starting at a point in an open and bounded set. The infinitesimal killing rate function depends on a control variable and parameters. Values of the control variable... more

The variational auto-encoder (VAE) is a deep latent variable model that has two neural networks in an autoencoder-like architecture; one of them parameterizes the model's likelihood. Fitting its parameters via maximum likelihood (ML) is... more

When seasonal time series are periodically integrated, we show that the any cointegration is either full periodic cointegration or full nonperiodic cointegration, with no possibility of cointegration applying for only some seasons. In... more

In this paper we extend the large-sample results provided for the augmented Dickey–Fuller test by Said and Dickey (1984, Biometrika 71, 599–607) and Chang and Park (2002, Econometric Reviews 21, 431–447) to the case of the augmented... more

This paper examines the implications of applying the Hylleberg, Engle, Granger, and Yoo (1990,Journal of Econometrics44, 215–238) (HEGY) seasonal root tests to a process that is periodically integrated. As an important special case, the... more